Overview

Forget all the mortgage acceleration programmes as they will cost you at least $1,000 - $2,000. The Mortgage Acceleration Calculator presents a Mortgage Acceleration Strategy that really works and it costs you nothing.

The first step of this Mortgage Acceleration Strategy is to shop around for a lender that can offer you such as:

- Full offset account facility

- Ability to make extra payments without fees or charges

- No redraw charges, especially when you go online for banking

It is critical that the home loan comes with a full offset account facility. This balance in the loan account is reduced by the amount held in the Offset account so the daily interest charged in the loan account is on a reduced balance. Eg. if the loan balance is $300,000 and the amount in the Offset account is $50,000 then the interest charged on the loan account is on the $250,000 ($300,000 - $50,000) and not the $300,000.

Once you purchase the Mortgage Acceleration Calculator you will get the full Mortgage Acceleration Strategy which will possibly save you thousands of dollars per year.

You will get $99 FREE bonus (shown in the table below and based on personal use price) when you purchase the Mortgage Acceleration Calculator.

| Free Bonus | Value |

|---|---|

| 1. Lifetime Free Update | $99 |

| Total Bonus | $99 |

Pay less if you DON'T need the bonus. Click here to learn how to pay less without bonus!

Here is a screenshot that will give you a better idea that what you need to do and what this Mortgage Acceleration Calculator can do for you.

Main Features

Here is a list of all the features provided by the Mortgage Acceleration Calculator.

1. A Mortgage Acceleration Strategy that really works and it costs you nothing;

2. Table and chart to show the offset benefits in time and costs (i.e. interest savings and time to pay off);

3. Allow you to specify loan repayment frequency (monthly, fortnightly, weekly) and change loan term, amount, interest rate;

4. Allow you to specify salary crediting frequency (monthly, fortnightly, weekly);

5. Allow you to specify weekly cash withdrawal from offset account;

6. Allow you to specify credit card interest free period (40 to 55 days);

7. Allow you to make additional weekly deposit and investment property rent deposit;

8. Allow you to have additional monthly one off payments;

9. Occasional deposit and withdrawal on a daily basis;

10. Allow you to estimate principal and interest home loans (P/I home loans) and interest only home loans (I/O loans);

11. Up to 30 years projection;

12. Allow you to enter the loan start date so the actual dates will be displayed along with the days being sequential numbers. Please refer to the screenshot below.

This Excel Mortgage Acceleration Calculator is a valuable tool for borrowers as it helps them to unnderstand how they can reduce the length and cost of their mortgage. Since mortgages typically span decades, even small extra payments towards the principal can have a significant impact on reducing total interest paid over time. By using this Excel Mortgage Acceleration Calculator, borrowers are able to see how they can use an Mortgage Acceleration Strategy to save money by essentially making extra payments towards the loan principal without increasing their regular home loan repayments.

This Excel Mortgage Acceleration Calculator not only makes financial planning easier but also allows for comparison between different repayment strategies. The chart in this Excel Mortgage Acceleration Calculator provides a visual comparison between a standard repayment schedule and an accelerated plan, showing how the Mortgage Acceleration Strategy allows the loan balance to decrease faster and reduce total interest paid.

This Excel Mortgage Acceleration Calculator is very flexible and comprehensive as it can handle complex scenarios including cash withdrawals, salary crediting, and up to 30 years of projection.

In essence, this Excel Mortgage Acceleration Calculator empowers borrowers to make informed decisions about their home loan repayment strategies and this can potentially save the borrowers thousands of dollars in interest and pay off their home loan much sooner.

Things You Need to Know

This calculator is built in Microsoft Excel worksheet. You need to have Microsoft Excel® 2013 & Above for Microsoft Windows® OR Microsoft Excel 2016 & Above for Mac® to use it.

All the calculators (paid and free ones) on this website are password protected. We don't provide unprotected versions of the PAID calculators due to copyright reasons. If you purchase the paid calculators because you want to get the unprotected version please don't make the purchase as we are not going to provide unprotected copies. By purchasing the paid calculators you agree that no unprotected copies of the PAID calculators will be provided to you. If you don't agree please do not purchase. If you need the unprotected version of any FREE calculator a fee will apply. The advantage of the unprotected version is that you can freely edit the tool without any limit although we still own the copyright of the unprotected calculator. Please note you cannot redistribute our calculators without a written approval from us even for the ones with your modification or customization. In addition we are not going to provide any support on unprotected calculators with any modification or customization.

What is a home loan/mortgage?

A home loan, or mortgage, is a loan paid off over an agreed term, which the property is held as security for. Almost half of all Australian properties have a mortgage against them, which means that getting a mortgage is a big part of how Australians achieve their home buying dreams.

A typical scenario of how the home loan works is listed below:

- A person wants to buy a $1.5m house – but they don't have enough money to pay it all upfront as they only have $300,000 deposit so they need $1.2m extra.

- They create a $1.2m mortgage with a lender (e.g. bank, credit union etc.), so the lender can pay the $1.2m to the seller immediately. The $1.2m is called the principal (the amount the person has borrowed).

- Now, the person must pay the lender back through regular mortgage payments – including interest. This could be monthly, fortnightly (most common in Australia), or weekly.

- After paying off the home loan, the person must formally discharge the mortgage to remove the lender from the property title. Following the successful mortgage discharge, an electronic certificate of title or paper title deed will be sent to the person. The person now owns the house.

There are many types of home loans. Please refer to the table below for more information.

Types of Home Loans

| Category | Type | Description | Key Notes |

|---|---|---|---|

| Loan Purpose | Owner Occupied (OO) | A property that the owner will live in. | Typically lower interest rates than investment loans. |

| Investment (IPL) | A property purchased to rent out to tenants. | Usually has higher interest rates than owner-occupied loans. | |

| Repayment Type | Principal & Interest (P&I) | Borrowers repay part of the loan principal (the amount the borrower has borrowed) plus interest. | Most common repayment structure. |

| Interest Only (IO) | Borrower pays only the interest during the interest-only period. | Maximum policy: usually 5 years (OO) and typically up to 10 years, sometimes 15 years (IPL). | |

| Interest Type | Standard Variable Rate | Interest rate can change depending on market conditions. | Repayments increase if interest rates rise. |

| Fixed Rate | Interest rate locked for a fixed period. | Break cost if repaid early; prepayment threshold applies during fixed term; optional rate lock fee. | |

| Split Loan | Loan divided between fixed and variable portions. | Balances risk and flexibility. | |

| Product Bundle | Basic/Value | Simple home loan with minimal features. | Often used by first home buyers. |

| Packaged | Home loan bundled with additional banking products. | May include fee waivers and an offset account. |

What is an offset account?

An offset account is a transaction account linked to the home loan (typically the variable rate home loan), which allows customers to reduce the amount of interest paid on their loan.

How does an offset account work?

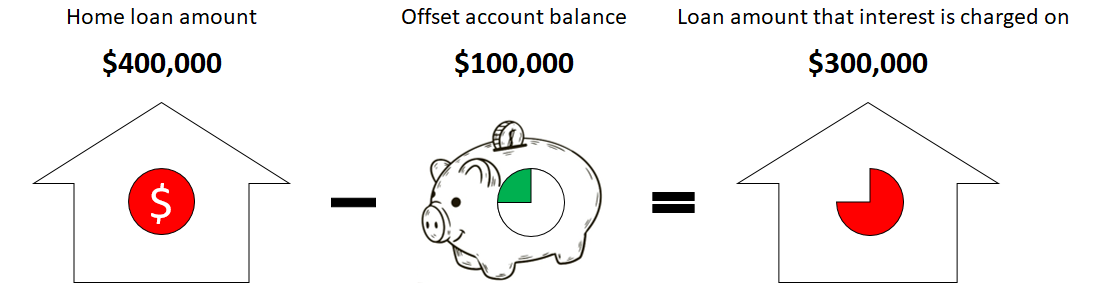

Each day the balance in the customer's eligible linked transaction account is offset against the amount owed on their home loan when calculating the interest. Interest is calculated daily and charged monthly only on the net amount, which is the loan balance less the transaction account balance for that day. This allows for customers to only pay interest on their home loan minus the balance of their offset. In other words, the deposits in the offset account reduce your home loan's interest on a dollar-for-dollar basis! This is how an offset account reduces your mortgage interest. The image below illustrates how an offset account works.

What's the difference between full offset account and partial offset account?

A full (100%) offset account uses every dollar in your offset account to reduce the loan balance interest is calculated on, typically on variable loans.

A partial offset account is either where only a portion of your money in the offset account is used to offset the home loan balance (e.g., a cap of $20k offset limit even if you have $100k in your offset account) or where a portion of your home loan account that is equal to the balance of your linked offset account is charged interest at a reduced rate (e.g. 1.89% p.a. instead of 5.79% the full rate) while the remaining balance of your home loan account is charged at the regular (full) home loan rate. A partial offset account is often linked to fixed-rate loans.

Most lenders in Australia do NOT offer offset accounts on fixed-rate loans although Bendigo Bank, Bank Australia, Qantas Money, and some smaller lenders do offer offset accounts on both fixed and variable loans.

Can I withdraw money from my offset account anytime?

Of course you can withdraw from your offset account anytime you need money! An offset account is basically a transaction account linked to your home loan. You can withdraw cash, transfer money, pay bills, and use a debit card etc.

Is an offset account better than making extra mortgage repayments?

Placing it in an offset account immediately reduces interest, but you can still withdraw it if needed. Making an extra repayment locks the money into the mortgage — good for discipline, but less flexible. Normally the extra repayments can be accessed through the redraw facility of your home loan. A redraw facility allows you to withdraw extra repayments made on your home loan. Usually available on variable-rate loans, the redraw facility allows you to access the extra repayments you make, but may come with fees or limitations on the number of withdrawals or a cap on how much you can withdraw (e.g. up to 80% of the extra repayments).

The table below shows the clean, side-by-side difference between offset account and redraw facility:

Offset vs Redraw (At a Glance)

| Feature | Offset Account | Redraw Facility |

|---|---|---|

| What it is | Separate transaction bank account linked to your loan | Extra repayments sitting inside your loan |

| Access to money | Anytime (like a normal account) | Usually accessible, but may have limits |

| Effect on interest | Reduces loan balance used to calculate interest | Reduces actual loan balance |

| Flexibility | Very high | Medium (depends on lender rules) |

| Fees | Often package/account fees | Usually free or low cost |

| Risk | Your money remains fully yours | Access can be restricted by lender |

In most cases, it does not matter whether you put your money into the offset account or your home loan account (redraw facility). However, if funds from an offset account or redraw facility are used to purchase an investment property, the financial implications can differ significantly.

Do all mortgage types allow an offset account?

No, not all mortgage types allow an offset account. While offset accounts are a popular feature for reducing interest payments, they are generally restricted to variable rate home loans. Sometimes, low-cost "basic" or "no-frills" variable loans do not offer the offset feature, as they are designed to have lower fees.

Most fixed-rate loans do not permit a linked offset account. Some lenders (e.g., Bendigo Bank) offer offset accounts on fixed-rate loans, but these may come with restrictions like lower offset percentages (partial offset) or limited offset amounts.

Are there fees or tax implications for using an offset account?

Yes, offset accounts often have fees, such as monthly account-keeping fees (around $5-$10/month) or annual package fees (up to a couple of hundred dollars). Many lenders will waive the fees for the first year. Bank employees typically receive fee waivers for the entire term of the home loan.

On the tax side, because you're reducing interest rather than earning interest, there’s no taxable income - unlike a savings account where interest earned is taxable. This can make offset accounts more tax-efficient than keeping money in a regular savings account.

A common misconception about investment property loans is that if you withdraw money from the offset account, the loan interest is only deductible if those withdrawn funds are used to produce assessable income. The reality is that withdrawing money from an offset account linked to your investment property loan for personal use (e.g., purchasing a new car) does not affect interest deductibility, as the loan balance and its purpose remain unchanged. With an offset, the loan balance stays the same and the loan's purpose doesn't change. Moving money in and out of the offset doesn't create mixed-purpose debt issues. You can still claim the interest you actually pay on the loan, based on its original purpose. In other words, when you withdraw money from the offset account for personal use, it does not need to be apportioned because the offset account itself is not the loan. In contrast, redrawing funds from the investment property loan for personal expenses alters the loan's purpose and reduces the deductible portion of the interest. This means that any money taken from the redraw facility came from the loan and it had to be apportioned.

The table below illustrates the differences between an offset account and a redraw facility in the context of withdrawing funds from an investment loan for personal use.

Offset vs Redraw Comparison

| Scenario | Offset Account | Redraw Facility |

|---|---|---|

| Investment Property Loan Balance | $500,000 | $400,000 |

| Interest Rate | 5% | 5% |

| Offset Account Balance | $100,000 | - |

| Money Available for Redraw | - | $100,000 |

| Interest Charged (Before Withdrawal) | ($500,000 − $100,000) × 5% = $20,000 | $400,000 × 5% = $20,000 |

| Interest Deductible (Before Withdrawal) | $20,000 | $20,000 |

| Withdraw for Personal Use | $100,000 | $100,000 |

| Interest Charged (After Withdrawal) | $500,000 × 5% = $25,000 | $500,000 × 5% = $25,000 |

| Interest Deductible (After Withdrawal) | $500,000 × 5% = $25,000 | $400,000 × 5% = $20,000 |

Common Issues with Offset Account

In this section we will discuss some common issues with offset account and share some tips to avoid the issues.

Check Linkage: Log into your bank app and confirm the account is formally linked to your mortgage.

Compare Costs: Calculate if the annual fee is less than the expected interest savings.